Information only. Nothing on this page constitutes financial, tax, or legal advice. Always seek advice from a qualified, regulated financial adviser before making any financial decision. Read our full disclaimer.

If you are a British expat with a UK pension, one date now matters more than most: 6 April 2027. From that day, most unused pension funds will count as part of your estate for UK inheritance tax for the first time. For decades, a pension was the one part of your wealth that sat safely outside the tax. That advantage is about to fall away, and the people most exposed are often those who built a plan years ago and have never revisited it under the new rules.

This guide is written for British nationals living abroad, whether you are settled in Spain, Portugal, France, the UAE, Singapore, Australia, the United States or anywhere else. It explains what actually changes, why living overseas no longer puts your pension automatically out of reach, the quiet double-tax trap that can catch families on later deaths, and the worked numbers that show why starting early is worth so much more than leaving it late.

Nothing here is advice. It is a clear, honest map of the territory, so you can decide whether your position is worth a proper look while there is still time to act.

What actually changes on 6 April 2027

Today, most defined contribution pensions, including SIPPs and most workplace money-purchase schemes, sit outside your estate when you die. Nominated beneficiaries can usually receive the unused fund with no inheritance tax, whatever its size. That is precisely what has made pensions such a powerful way to pass wealth on.

From 6 April 2027, that changes. Most unused pension funds and lump-sum death benefits will be brought inside the estate for inheritance tax. The value of the pot at the date of death is added to the rest of your estate, and anything above your available allowances is taxed at the standard 40% rate.

The change was announced in the Autumn 2024 Budget and has since been confirmed, with draft legislation and HMRC guidance published. The direction of travel is settled. What remains open for many expats is whether they have looked at what it means for them.

Does it even affect you? The allowances that decide it

Inheritance tax is not charged on everything you own. It applies only to the value of an estate above your allowances:

The nil-rate band: £325,000 per person.

The residence nil-rate band: up to a further £175,000 per person, where a main home passes to direct descendants (this tapers away for larger estates).

A married couple or civil partners can combine their allowances, so a surviving partner's estate can often pass on up to £1,000,000 before any tax is due.

Below those thresholds, there is generally no inheritance tax to pay. In fact, HM Revenue and Customs expects that more than 90% of estates will still pay no inheritance tax even after these changes. Of the estates with inheritable pension wealth, around 10,500 a year are expected to become liable for inheritance tax that would not have been before, roughly 1.5% of all UK deaths. (Source: HMRC technical note: Inheritance Tax on pensions, November 2024, updated following Finance Act 2026.)

So why does it matter for so many expats? Simple arithmetic. A home, savings and a decent pension added together climb past those frozen thresholds far more easily than people expect, and the pension being counted from 2027 is often the single piece that tips an estate over the line.

"But I live abroad." The residence-based trap most people miss

Here is the part that catches British expats out, and where a lot of older guidance, and even some adviser articles, are now simply out of date.

For decades, your exposure to UK inheritance tax was governed by domicile, a slippery legal concept tied to your long-term home. That system was scrapped on 6 April 2025. The UK now runs a residence-based test instead.

Under the new rules, you are a long-term resident for inheritance tax if you have been UK tax resident for at least 10 of the previous 20 tax years. If you are a long-term resident, your worldwide estate is within the scope of UK inheritance tax, and that includes your UK pension from 2027.

Crucially, the exposure does not vanish the moment you move abroad. It follows you for a while, through what advisers call the IHT tail:

If you were UK resident for 10 to 13 of the last 20 years, you remain a long-term resident for 3 years after leaving.

The tail lengthens with the years you spent in the UK, up to a maximum of 10 years after departure for those resident the longest.

Only once you have been non-resident long enough to fall outside the test does UK inheritance tax narrow to your UK-situated assets alone.

The practical message is blunt: living in Lisbon, Dubai or Sydney does not, by itself, put your UK pension beyond UK inheritance tax. Whether it does depends on your residence history and the tail, and that is exactly the kind of technical question only a regulated specialist can answer for your specific circumstances.

The quiet double-tax trap on later deaths

This is the wrinkle very few people know about, and the one that can sting families most.

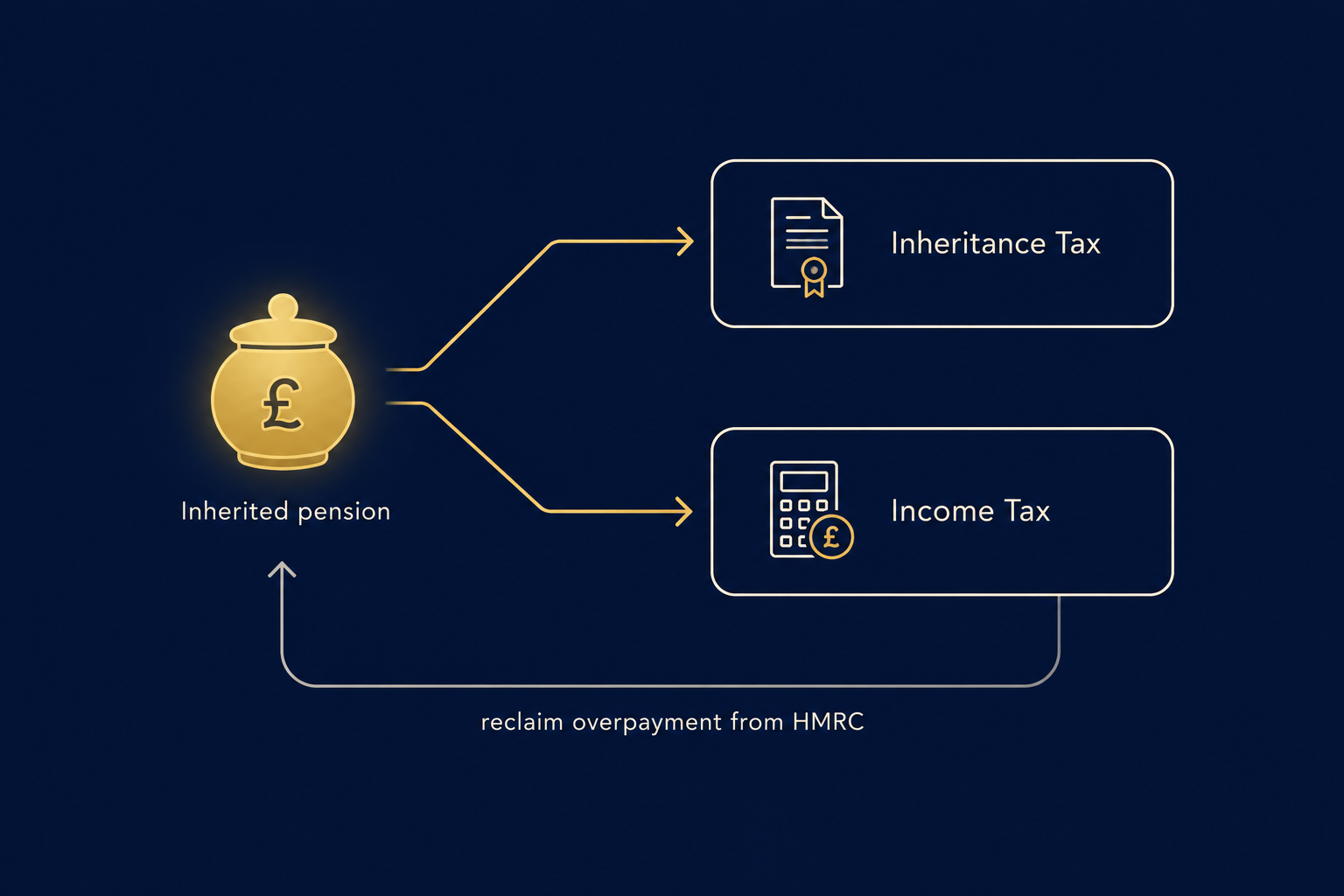

Where someone dies after age 75, the beneficiaries of an inherited pension already pay income tax on what they draw from it, at their own marginal rate, which can be up to 45%. From April 2027, that same pension may also be counted for inheritance tax. In other words, one pot, potentially touched by two taxes.

In principle, the rules are designed to prevent genuine double taxation. HMRC's stated position is that inheritance tax is calculated first, and income tax then applies only to what remains, with relief for the portion that has borne inheritance tax. That is the theory.

In practice, advisers expect the early years to be messy. The process involves the pension scheme, the personal representatives of the estate and HMRC all at once. Timing mismatches around valuations and deadlines make it quite possible for families to pay first and reclaim later, with reclaims potentially taking months. Some advisers have described "painful teething challenges" while the system beds in.

None of this is a reason to panic. It is a reason to make sure that whoever will one day handle your affairs is not left to untangle it under pressure, at the worst possible time. A clear plan, made in advance, is far easier than a reclaim made in grief.

What it could look like: three illustrative estates

Numbers make this real. The scenarios below are illustrative only. They are not forecasts, not advice, and the people are not real. They assume a single person (so one set of allowances) who is a UK long-term resident with worldwide assets in scope, and they ignore the residence nil-rate band for simplicity. Your own position could be very different.

Non-pension estate + pension pot

IHT before 6 Apr 2027

IHT from 6 Apr 2027

£300,000 + £150,000 pension

£0

£50,000

£500,000 + £400,000 pension

£70,000

£230,000

£700,000 + £600,000 pension

£150,000

£390,000

Those are increases of £50,000, £160,000 and £240,000 respectively, driven entirely by the pension now being counted. The pattern is consistent: the larger and more untouched the pension, the more the 2027 change adds to the eventual bill. For an expat who left the UK years ago with a substantial SIPP that has quietly compounded ever since, the pension can become the single biggest source of inheritance tax in the estate.

The real cost of waiting

Most of the money lost to inheritance tax is not lost to bad planning. It is lost to no planning, by people who fully meant to get round to it.

Independent economic modelling for Octopus Investments, carried out by the Centre for Economics and Business Research, found that affluent families who begin estate planning at 50 could pass on around £400,000 more on average than those who wait until 70. Across the country, the firm estimated that once pensions enter the net, up to £12.3 billion of inheritance tax stands to be paid simply because planning starts late, or never starts at all.

The reason is simple: many of the most effective steps need time to work. A gift made today starts a seven-year clock. Allowances reset on a multi-year cycle. Structures take time to arrange properly. The window to look calmly, rather than react under pressure, is open now and narrows with every month.

The national picture tells the same story. UK inheritance tax receipts reached a record £8.5 billion in 2025/26, and the Office for Budget Responsibility forecasts they will rise to roughly £14.5 billion by 2030/31. Much of that increase is made of ordinary families crossing the line without realising, frozen allowances and rising asset values doing the quiet work.

What still protects your family

The picture is not all loss. Several long-standing protections remain firmly in place:

A pension or estate passing to a surviving spouse or civil partner is still generally exempt, with no limit.

Gifts to charity continue to be exempt.

Death-in-service benefits and some annuities sit outside the new rules.

The usual allowances, exemptions and reliefs around estate planning still apply, including the seven-year rule on lifetime gifts.

What these have in common is that they reward planning and punish delay. They are not switches to flick at the last moment. Most need to be arranged while there is still runway ahead of you, which is exactly why understanding your position early matters so much. Which of them apply to you, and how, is a question for a regulated specialist who knows your full circumstances and your country of residence.

Who is looking at the whole picture?

Your UK pension, your wider estate, your income, and the fact that you are tax-resident in another country were never meant to sit in separate boxes. A change in one affects all the others. The interaction between UK inheritance tax and your life abroad, including any inheritance or succession tax in your country of residence and any double-tax treaty between the two countries, is exactly the kind of thing that falls through the gap when no one is looking at it together.

That joined-up view is the most valuable thing a good review offers, and the first thing to disappear when a pension is simply left to run. You do not need to have the answers. You only need someone qualified to look at everything at once, through the lens of a British expat settled where you live, rather than as a generic file that happens to be abroad.

Your seven-question self-check

A quick way to gauge where you stand. Count how many you can answer with genuine confidence.

Do I know the current value of all my UK pension pots, across every scheme?

Once the pension is counted, does my estate sit below the allowances, or above them?

Do I understand whether I am still a UK long-term resident, and where I am in the IHT tail?

Would my family know how to handle the tax on an inherited pension correctly, rather than overpay and reclaim?

Has my plan been reviewed under the 2027 rules, not the old ones?

Do I know which exemptions and reliefs still apply to my situation?

Is anyone looking at my pension, my estate and my life abroad together?

If you answered most of them confidently, you are well prepared, so keep it that way. A few blanks is completely normal and worth a closer look. If most are blank, a review before 2027 is one of the kindest things you can do for the people you love.

How Pharos Introductions helps

Pharos Introductions does not give financial, tax or legal advice, and never will. What we do is connect qualifying British expats with a regulated specialist suited to their situation, so the review is carried out properly by someone qualified to do it. Our UK inheritance tax planning for expats service page sets out what a review typically covers. The introduction is ours to make. Every decision after that stays firmly with you. There is no cost for the introduction and no obligation to proceed.

The simplest place to start is the free IHT calculator. A few details, and you will see roughly where your estate sits against the threshold under the 2027 rules, before you decide whether to take it further.

Do the April 2027 pension changes apply to me if I no longer live in the UK?

They apply to UK-registered pension schemes, including SIPPs and most workplace defined contribution schemes. Whether inheritance tax actually bites in your case depends mainly on your residence position under the rules that began on 6 April 2025. If you have been UK tax resident for at least 10 of the last 20 tax years you are a long-term resident, and your worldwide estate, including your UK pension, is within scope. After leaving the UK an "IHT tail" of up to 10 years can apply. This is a technical assessment that a regulated specialist should make for your circumstances.

I have a SIPP I have not touched since leaving the UK. Am I affected?

If you hold an undrawn SIPP and you are still a UK long-term resident, the value of that SIPP will likely be included in your estate for inheritance tax from April 2027. How much, if any, tax results depends on the size of the pot, your other assets, and the allowances available to your estate. A specialist can model the projected liability and explain what options exist.

What is the double-tax issue on pensions after age 75?

Where death occurs after age 75, beneficiaries already pay income tax on money they draw from an inherited pension, at their own marginal rate. From April 2027 that pension may also be counted for inheritance tax. The rules are designed so that inheritance tax is charged first and income tax applies only to the remainder, to avoid true double taxation. In practice, advisers expect administrative friction in the early years, with some families paying tax up front and reclaiming overpayments from HMRC later. Planning ahead reduces the risk of that friction landing on your family.

Does this affect defined benefit (final salary) pensions?

The position differs from defined contribution schemes. Final salary pensions typically pay an income during retirement and, after death, may continue as a reduced pension for a spouse or dependant, rather than passing as a lump-sum fund. The 2027 changes are aimed primarily at unused defined contribution funds and lump-sum death benefits. If your defined benefit scheme has a significant lump-sum death benefit, it is worth having a specialist check whether there is any exposure.

How does UK inheritance tax interact with the taxes in my country of residence?

Many countries levy their own inheritance, estate or succession taxes, and a small number have double-tax treaties with the UK that affect how the two systems interact. The combined effect varies significantly by country. If you live somewhere with its own succession tax, the interaction of both regimes on the same assets is something a specialist should model as part of any review, to avoid being taxed twice on the same money.

Is it too late to do anything before April 2027?

No, but some of the most effective steps need time to work, so the value of acting is highest now and falls as the deadline approaches. A thorough review of pension valuations, beneficiary nominations, wills and the order in which you draw assets takes time to do properly. Starting the conversation now, rather than in early 2027, is the difference between having genuine choices and having fewer of them.

This guide is for general information and education only. Nothing in it, including any figures, examples or tools, constitutes financial, investment, tax or legal advice. Pharos Introductions is an introducer. We are not a financial adviser and are not authorised or regulated as one. We do not provide advice, nor do we assess the suitability of any product or arrangement for any individual. Any figures and scenarios are illustrative, are not a forecast or guarantee, and depend entirely on individual circumstances and the law as it currently stands, which may change. Where we introduce you to a regulated specialist, any engagement is a direct relationship between you and them. This guide is not directed at residents of the United Kingdom, and we do not market our services to people ordinarily resident there. Only a regulated adviser with full knowledge of your circumstances can make a recommendation suited to you.

Sources

HM Revenue and Customs, Technical note: Inheritance Tax on pensions (GOV.UK), and the Autumn 2024 Budget announcement.

HM Revenue and Customs, Inheritance Tax if you are a long-term UK resident (GOV.UK), setting out the residence-based rules from 6 April 2025 and the 10-of-20-years test.

Which?, Inheritance tax on pensions: how the new rules will work in practice.

Office for Budget Responsibility, public finances and inheritance tax receipts forecasts.

Octopus Investments, 50nomics: the evidence behind earlier estate planning, with economic modelling by the Centre for Economics and Business Research.

This article is for informational purposes only and does not constitute financial, tax, or legal advice. Please seek specialist regulated advice for your individual circumstances.